USD/JPY Forecast: Dollar faces trust test as Moody’s downgrade compounds haven doubt

- USD/JPY correlations with rates and risk assets have broken down

- USD behaving more like a risk asset than a safe haven

- Moody’s downgrade highlights growing concerns over U.S. fiscal outlook

- Japan’s April CPI looms as key event risk this week

- Momentum signals turning, with downside levels back in focus

Summary

USD/JPY’s traditional drivers—rate differentials and risk appetite—have gone missing, with recent price action showing little correlation to bonds or equities. Instead, the pair is behaving more like a barometer of confidence in the U.S., just as Moody’s joins S&P and Fitch in downgrading its sovereign rating. With the dollar already being sold on strength, the move could reinforce doubts over its haven credentials. Japan’s inflation data and U.S. debt concerns loom large, with technicals offering key signposts as the macro environment gets murkier.

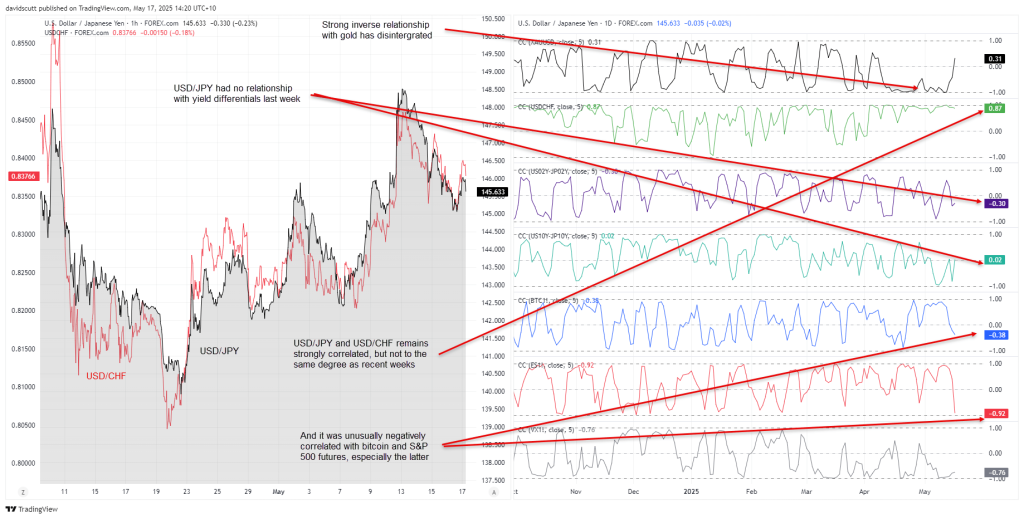

USD/JPY Correlations Break Down

USD/JPY is known for its historical relationship with interest rate differentials and risk appetite, but those drivers are nowhere to be seen at present. The correlation coefficient scores below underline that point, revealing no major relationship between USD/JPY with either short or longer-dated interest rate differentials between the United States and Japan, and unusual inverse correlation with riskier asset classes such as bitcoin and S&P 500 futures. Curiously, the ultra-tight relationship with gold has totally disappeared, while its relationship with the Swiss franc and VIX futures has also started to weaken.

Moody’s Move May Pressure USD Further

That point is important in the context of Moody’s decision to strip the United States government of its prized Aaa rating late Friday, reducing it to the second-highest rung of Aa1 with a stable outlook. The decision really comes as no surprise, especially as S&P and Fitch—the other two main ratings agencies—had already done the same in 2011 and 2023 respectively.

And to be frank, looking at trends in the U.S. trade balance, federal debt accumulation and the debt-to-GDP ratio, you could ask why the move didn’t arrive much sooner.

Source: Forex